Garmin Ltd. (GRMN) Stock Analysis

1. Summary

- Garmin Ltd (ticker: GRMN) is a manufacturer of wireless devices in the segments fitness, outdoors, automotive, marine and aviation.

- For the current share price of 105.54 USD our DCF model yields 13% possible upside, for the stock while providing medium risk for shareholders.

- Market cap: 20B USD, P/E: 19.0, P/B: 13.3, EV/EBITDA: 14.0, Dividend Yield: 2.47%

- we came across this company through a screening on our site StocksOnView, which is currently in open beta and free to use

2. Company Overview

Garmin Ltd. designs, develops, manufactures, markets and distributes wireless devices, mainly for people living an active lifestyle.

2.1 Segments

The company serves five main markets: fitness, outdoor, aviation, marine and automotive. Many of the products use global navigation satellite systems such as GPS, for each market the company aims to position itself as a premium supplier.

2.1.1 Fitness

Products in this category include running and multisport watches, smartwatches, cycling products such as GPS bike computers, the “Garmin Connect” mobile app that lets you track and compare your performance with others, and the “Connect IQ” platform that lets you connect your Garmin devices with third-party apps. The major competitors in this segment are Amazon, Apple, Bryton, Coros, Elite, Fitbit (Google), Huawei, Polar, Samsung, Suunto, Wahoo Fitness, Whoop, Xiaomi, and Zepp Health. In 2021, this market accounted for 31% of revenue. However, in Q1 of the new fiscal year, revenues declined 28% (y/y), which management attributes to a relatively strong prior year.

2.1.2 Outdoor

Outdoor products include handhelds, satellite communications, adventure watches, GPS navigators and solutions for sporting dogs such as tracking collars. The relevant competitors are Casio, Coros, Dogtra, Globalstar, Shearwater Research, SportDOG, Suunto, TAG Heuer, Tissot, Trackman, Vista Outdoor and Zoleo. In 2021, 26% of the companies’ revenue was generated in this market. In the last quarter, the company also managed to increase this metric by 50% (y/y), with an operating margin of 39%, mainly due to the launch of the fénix 7 and instinct 2 series (premium smartwatches).

2.1.3 Aviation

Products in this sector include integrated flight decks, electronic flight displays, navigation and communication devices, automatic flight control systems and more. Major competitors are Aspen Avionics, CMC Electronics, Dynon Avionics, ForeFlight, Genesys Aerosystems, Honeywell Aerospace & Defense, Innovative Solutions and Support Inc, L-3 Avionics Systems, Collins Aerospace, Safran, Thales, and Universal Avionics Systems Corporation. 17% of the companies’ sales came from this market in 2021, and this metric was virtually unchanged year-over-year in the first quarter.

2.1.4 Marine

Products in this market include fish finders, sonar, radar, chartplotters, antennas and more. Its main competitors are Furuno, Johnson Outdoors, Navico and Raymarine and by 2021 they generated 14% of their revenue in this market. In 1Q2022, the company managed to increase the corresponding revenues by 21% (y/y) with an operating margin of 23%.

2.1.5 Auto

Products in the Automotive category mainly comprise navigation systems and dashcams. In 2021, they accounted for 12% of the company’s sales, which increased by 11% (y/y) by the first quarter of 2022. Future investments are planned primarily in this area, with the aim of entering into long-term partnerships with established car manufacturers. One such partnership is already in place with BMW, where Garmin navigation devices will be installed in the BMW 7 Series from the second quarter of 2022. Besides that they also have an ongoing partnership with Peugeot. In order to generate added value for shareholders, it is very important that the investments lead to further such collaborations. Competitors in this market include Rand McNally, TomTom, Alpine Electronics, Aptiv, Bosch, Continental, Harman International Industries, the Mitsubishi Group and Panasonic Corporation.

2.2 Management & Culture

Garmin was founded in 1989 by Gary Burrell and Min Kao. Min Kao has a PhD in electrical engineering, he was CEO until 2021 and is now executive chairman. He and Jonathan Burrell, Gary Burrell’s son, each own about 10% of the company. Jonathan Burrell worked for the company as a mechanical engineer since 1990 and is now a member of the board of directors.

The CEO is Cliften Pemble, who has a bachelor’s degree in mathematics and computer science and started as a software engineer at Garmin in 1989. He was the company’s 13th employee and has been CEO since 2013. Chief Financial Officer Douglas Boessen joined the company in 2014 after working for Collective Brands for 15 years and for Arthur Andersen for 13 years before that.

Garmin currently employs around 18000 people worldwide. The company is rated at 4 out of 5 stars on the employer review site Glassdoor.

3. Risk

3.1 Qualitative

Garmin mostly operates in the premium market for retail customers. Their products have stellar reviews online and get a lot of coverage from reviewing and blogging sites, indicating a loyal customer base, but the market is highly competitive.

To stay ahead of the competition Garmin spends a lot on research and development. To date they hold over 1700 patents and 1000 trademarks.

In 2021 they suffered from supply line issues, which motivated them to increase their inventory. This increase significantly reduced their free cash flows in the first two quarters of 2022.

Four out of ten of their manufacturing facilities are located in Taiwan and one in China exposing them to geopolitical risk.

Most members of the executive team have been with the company since its inception and have made it one of the largest companies in its market, demonstrating their capabilities.

We conclude the qualitative risk for Garmin to be medium-high.

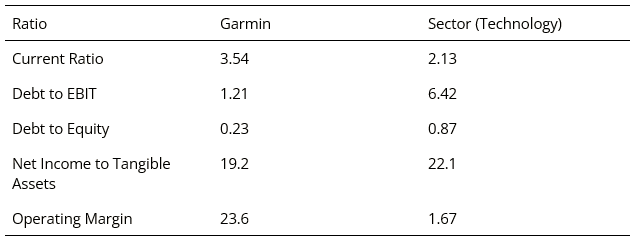

3.2 Quantitative

To assess the quantitative risk, we look at five ratios that we believe are good illustrations of the robustness of the company’s business model.

We conclude the quantitative risk for Garmin to be low.

3.3 Summary

Qualitative: medium-high

Quantitative: low

We conclude that shareholders of Garmin face medium risk.

4. Monte Carlo Analysis

To estimate a fair value for Garmin we perform a monte carlo simulation of discounted cash flow calculations. This method is adopted from Aswath Damodaran, a professor of finance at NYU (explained in the book ‘The Dark Side of Valuation’ or here: https://youtu.be/rFd_qEpYFBc).

We simulate 5 years of cash flows discounted back to today and apply a terminal multiple to our last simulated cash flows.

In the following we discuss our used input variables.

4.1 Growth

Over the last 5 years Garmin grew its revenues at an average annual growth rate of 11% with a standard deviation of around 7%.

The wearable technology market is estimated to grow at 18% annually in the next 4 years (Source: https://www.marketsandmarkets.com/Market-Reports/wearable-electronics-market-983.html). The automotive infotainment market is expected to grow at 8.4% annually in the next 5 years (Source: https://www.marketresearch.com/IMARC-v3797/Automotive-Infotainment-Global-Trends-Share-30835731). Garmin already has a high market share in most of its segments, so for the simulation we assume an annual revenue growth that is normally distributed with a mean of 8% and a standard deviation of 10%.

4.2 Margin

For Garmin’s operating margin we assume a triangular distribution with a peak at its 5 year average of 24% and ranging from 20% to 28%.

4.3 Terminal Multiple

The historical average of Garmin’s enterprise value to EBIT ratio is 18 and it’s currently trading at 16. In the Technology sector the current median enterprise value to EBIT ratio is 22. We will be using an enterprise value to EBIT ratio of 15 as our terminal multiple applied to the discounted cash flows of the last (5th) period.

4.4 Discount Rate

One method of determining an appropriate discount rate is to use the weighted average cost of capital (WACC). The WACC uses the capital asset pricing model, which in turn uses the stocks beta, a measure for its volatility in relation to the market. We don’t think that volatility is a great measure for risk, which is why we don’t use WACC.

We want our discount rate to be higher than the average market return, since we expect our investments to outperform and we want to be able to easily compare different investments. We are using a discount rate of 10% for all our investments.

4.5 Results

The monte carlo simulation yields the fair value of Garmin shares to be 119 USD. For the current share price of 105.54 USD we calculate up to 13% possible upside for the stock.

On our own behalf

All quantitative analysis is done via our website https://www.stocksonview.com, which we created to make the tools we use accessible to everyone. Many tools are free of charge, for some you will need a subscription. If you are interested and / or want to support us, we would be very happy to see you there. We are currently in open beta and all our premium features are available for free.

Disclaimer

Information is provided ‘as-is’ and solely for informational purposes, not for trading purposes or advice, and is delayed. No guarantee is given for the correctness of the information contained in this article.